The Myth of Low-Tax America: Why Americans Aren’t Getting Their Money’s Worth

By Steven Hill, The Atlantic, April 15, 2013

Today, in an annual rite of bemoaning government intrusion into our personal finances, most Americans can at least console themselves in their belief that the US has one of the lowest tax rates among developed countries.

Is that really true?

On the one hand, yes, we pay less. The share of our total national income captured by the government in taxes is small compared to most developed economies. On the other hand, we get less. Americans pay out nearly as much as some European countries, Canadians, and the Japanese. But we receive a lot less for our money.

Look at high-tax Sweden, which has the fourth-most competitive economy in the world, ahead of the U.S., according to the World Economic Forum. In return for paying their taxes, Swedes have access to a generous support system for families and individuals that most Americans can only dream about. That includes not only quality health care but also child care, a more generous retirement pension, low-cost college education (most Swedish universities charge no tuition fees), job retraining, paid sick leave, paid parental leave (after a birth or to care for sick children), ample vacations, affordable housing, senior care and more.

In order to receive the same level of benefits as Swedes, Americans have to fork out a lot more in out-of-pocket payments, in addition to our taxes. These payments often are in the form of fees, surcharges, higher tuition, insurance premiums, co-payments and other hidden charges. Whether it’s in the form of a tax, fee or surcharge, either way it comes out of your pocket. Yet that fuller picture is not considered when calculating who pays the most.

Here are examples where Americans are paying more than we realize, yet not getting our money’s worth:

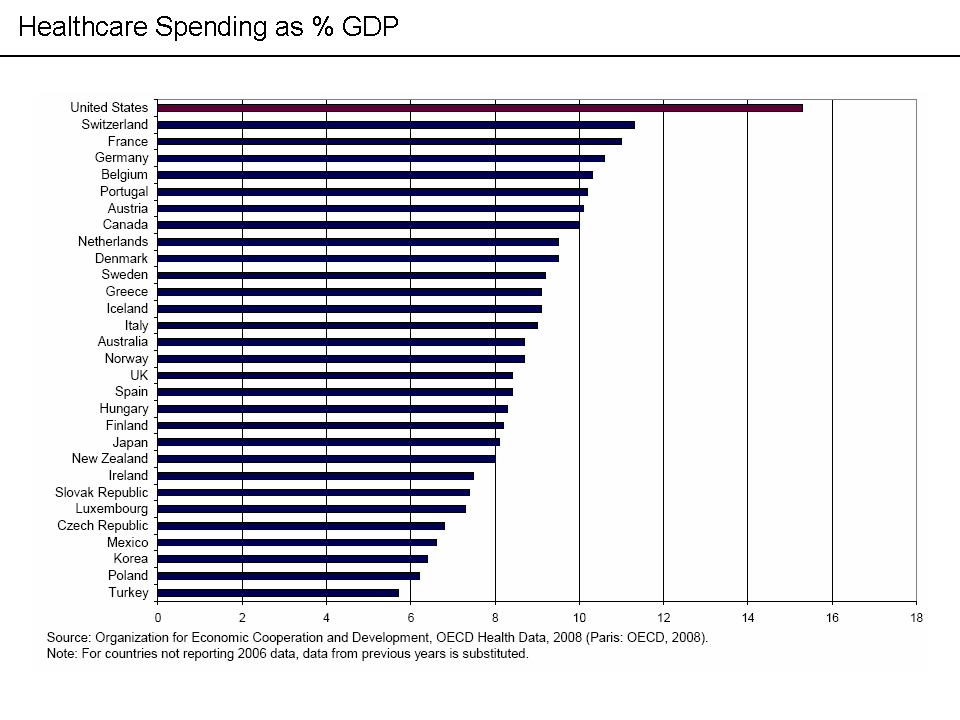

Health care. Compare what Americans pay on health care to what they pay in Japan – about twice as much money, whether measured per capita or as a percent of gross domestic product. For those Americans that have health care coverage (about 45 million of us still don’t), we continue to pay escalating premiums and deductibles. Many Americans are choosing to pay ridiculously high deductibles in order to reduce their premiums; I have a friend who bought a health care policy for his family of three children with a $10,000 a year deductible in order to keep his premiums affordable. But the Japanese receive health care in return for a modest amount deducted from their paychecks. And the various metrics show that they have better health, and their coverage is universal – everyone in Japan has health care, even as they pay less money to provide it.

{kind=link}

College education. Many Americans are frantically stuffing tens of thousands of dollars into various private savings vehicles for their children’s college education. Yet most German or Austrian students pay little in the way of tuition. Which means they don’t graduate from college with a huge debt burden of tens of thousands of dollars, like many U.S. students do.

Child care. Child care in the United States costs more than $12,000 annually for a family with two children. In some countries in Europe, child care is free. In others, they pay $1000-$2000 per year, depending on their income. So they are paying at most only one-sixth of what Americans are paying — and the quality is far superior.

Retirement. Millions of Americans are stuffing as much as possible into their IRAs and 401(k)s (which lost 40% of their value during the economic collapse in 2008) because Social Security provides a measly amount towards retirement — only about 33-40 percent of one’s final salary, which is not enough income for a comfortable retirement. It’s also quite a bit stingier than most other developed countries, with the average retirement replacement wage for member countries in the Organization for Economic Cooperation and Development (OECD) being 57%, and in the European Union 62%. Naturally a higher replacement wage better ensures that seniors don’t suffer a severe drop in their living standards, and for Americans to match that we have to save a lot more out of our own pockets.

Senior care. According to the OECD, Americans’ private spending on old-age care is nearly three times higher per capita than in Europe because Americans must self-finance a significant share of their own senior care by paying out-of-pocket. Whether it’s through taxes or out-of-pocket, either way, you pay.

Paid sick leave, paid parental leave. Without mandatory paid sick leave or parental leave (after the birth of a child), most Americans must self-finance their own time off. That’s money lost, out-of-pocket. But Canadians, Australians, Japanese and Europeans receive all of these and more — in return for their taxes.

Americans also tend to pay more in local and state taxes, as well as property taxes. Americans also pay hidden taxes, such as $300 billion annually in federal tax breaks given to businesses that provide health benefits to their employees — that’s $1000 for every man, woman and child in the United States, 45 million of whom don’t have any health coverage at all. That amount could go toward financing a real universal health care system covering every American, since it’s already coming out of every tax-paying American’s pocket.

The Bigger Picture of Our Tax Burden A thorough “tax analysis” would need to create a ledger in which all the supports and services Americans receive are listed on one side of the ledger, and the amount of taxes and any additional out-of-pocket expenses, fees and surcharges we pay are listed on the other. And then compare that to what other countries pay and what they receive. When you sum up the total balance sheet, it turns out that Americans pay out as much as those “high-taxed” Europeans — but we get a lot less for our money.

Unfortunately these sorts of complexities are not calculated into simplistic analyses like Forbes’ annual Tax Misery Index, which shows European nations as the most “miserable” and the low-tax United States happy as a clam down near the bottom on their index — right next to Indonesia, Malaysia and the Philippines. That’s because the Forbes Tax Misery Index only takes into account income tax, Social Security or retirement tax, corporate tax, sales tax or VAT and a few other minor taxes. It doesn’t consider the vast amounts that Americans are paying out-of-pocket, nor what people are receiving for those payments in terms of supports for families and individuals.

Ideologically-bound Americans counter that, at least in the U.S. it is discretionary about whether or not you purchase these services. The government isn’t picking your pocket through higher taxes or forcing you to purchase any particular form of assistance. That’s undeniably true. But in this economically insecure age, are services like health care, higher education or some kind of skilled job training, child care, sick leave, parental leave, retirement and senior care really discretionary? Or are they increasingly essential to ensure healthy, happy and productive families and employees?

An extreme tax-phobic position also ignores sound economic arguments about the most efficient way to organize the agencies and bureaucracies that people increasingly depend upon. Because the Germans, Swedes, Canadians and Japanese collect sufficient revenue via taxes, they can use that money to design comprehensive webs of “social insurance” — health care, child care, university education, senior care, and so on — in a way that allows them to reach economies of scale and design more cost-effective bureaucracies. They often do this in partnership with the private sector, and they can offer these services for a lot less money per capita than we can in the U.S., with our very decentralized, hodgepodge systems that are inefficient and comparatively expensive. That’s why Americans pay more per capita for health care, child care, university education and more. And that makes U.S. businesses less competitive compared to many of their international counterparts.

‘If Americans Knew What Swedes Receive For Their Taxes’ In the United States, any discussion of taxes revives age-old arguments about individualism vs. collectivism: to what extent should government be invested with the power to take from one person’s pocket and place money into another’s? Should the wealthy have to share a portion of their wealth with those less fortunate? The idea of “forced sharing” is one of the bright dividing lines of politics, both today and yesteryear.

But in most of the rest of the developed world these dilemmas have been more or less settled, and with a different outcome. For the most part, people don’t view taxes as collectivism steamrolling over the individual. Rather, taxes are viewed as a kind of membership dues that self-interested individuals pay to be in a club from which they all mutually benefit. A Labor Party leader in the Netherlands, Wouter Bos, captured the prevailing philosophy, arguing that the Dutch workfare support system is based on “enlightened self-interest” — “We all run the same risks, so we might as well collectively insure ourselves against those risks.”

Interestingly, an American acquaintance of mine who lives in Sweden told me that one evening, quite by accident, he and his Swedish wife were in New York City and ended up sharing a limousine to the theater district with a U.S. Senator and his wife. This Senator, a conservative, anti-tax southern Democrat, asked my acquaintance about Sweden and swaggeringly commented about “all those taxes the Swedes pay.” To which this American replied, “The problem with Americans and their taxes is that we get nothing for them.” He then told the senator about the comprehensive services and supports that Swedes receive.

“If Americans knew what Swedes receive for their taxes, we would probably riot,” he told the Senator. The rest of the ride to the theater district was unsurprisingly quiet.

Such American suppression of this important discussion only serves to perpetuate many myths and prevents Americans from understanding the vast shortcomings of our approach toward taxation. Consequently, millions of hard-working Americans never have the opportunity to enjoy such a comprehensive level of support for themselves and their families, unless they can pay a ton of money out-of-pocket — which most can’t afford.

Or unless they are a member of the United States Congress, who spare themselves nothing, and provide European-level support for themselves and their families, even as they pull up the drawbridge for the rest of us.